Structuring Your Giving Part 2: Choosing the Best Structural Form(s)

Jul 06, 2022Figuring Out Which Giving Structures Make the Most Sense for You

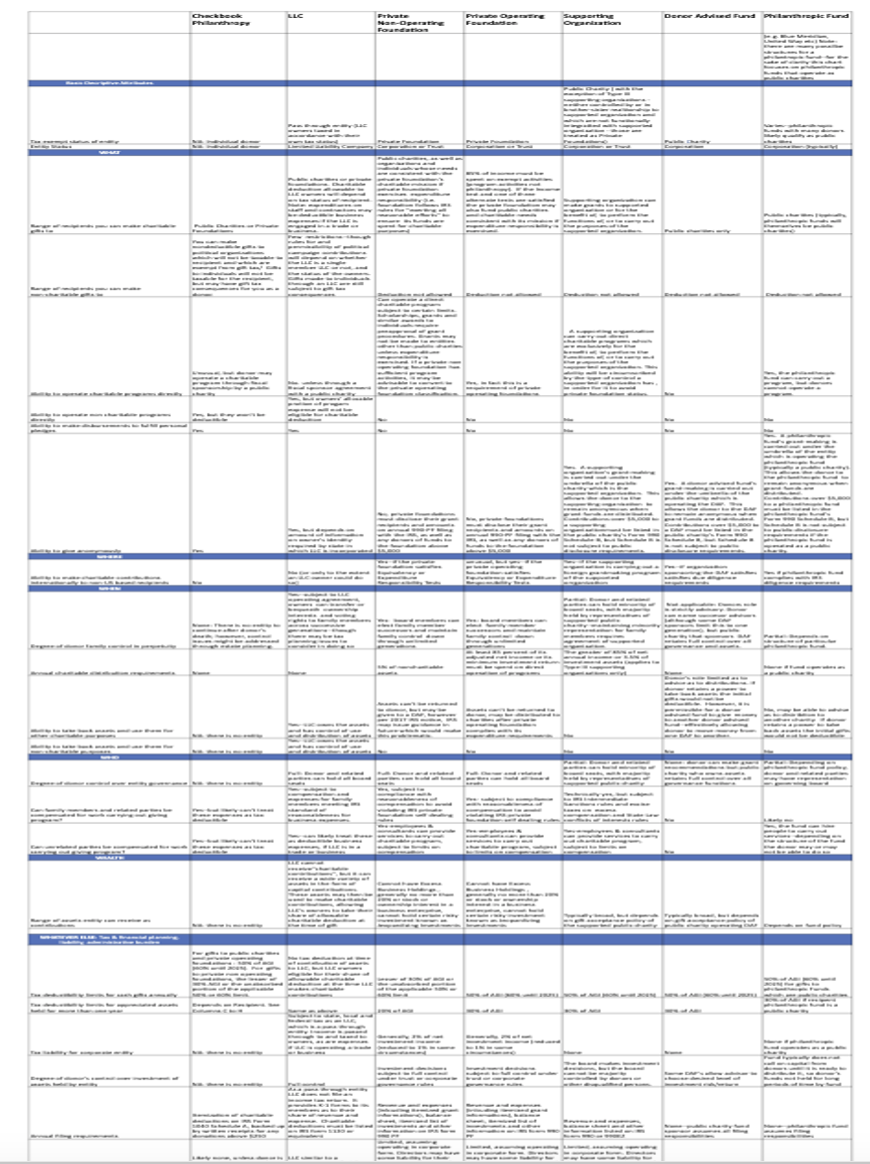

There’s a lot to consider as you try to figure out which giving structures are the best match for carrying out your giving. Here’s what I recommend: begin by identifying which of the key functional questions reviewed in this post are most relevant to your giving. Then consult the corresponding sections of this summary chart to see which of the 7 structural forms (checkbook philanthropy, donor advised fund, private foundation etc) are the best fit.

You can download a full size version of this table here.

You’ll still need to do your diligence and consult your financial and legal advisors before making your own decisions, but this chart is great for getting the big picture with a side by side view of the different features and attributes for the 7 main structural options for your giving:

- Checkbook philanthropy

- LLC

- Private non-operating foundation

- Private operating foundation

- Supporting Organization

- Donor-Advised Fund

- Philanthropic Fund

Key Functional Questions

WHAT—What strategies can you carry out?

Range of recipients to whom you can give charitable grants

What’s the issue here? Some giving structures, such as donor-advised funds, only allow you to give to entities that are established as public charities. You’ll need to use a different structure if you want to make tax-deductible grants to individuals, such as for scholarships, or for direct income support. This restriction also applies to any other entities that are not incorporated as public charities. For example, you cannot use a donor-advised fund to pay a consulting firm carrying out research related to your giving program.

Range of recipients to which you can give non-charitable grants

In some cases, your giving program might include supporting an activity that is not charitable. You might even have plans for things which are prohibited or limited for 501(c)(3) organizations, such as political campaign activity and certain kinds of issue advocacy. In many cases, donors simply engage in this kind of non-deductible giving by utilizing their personal funds. If you want to be able to carry your philanthropy out through an organizational structure, you’ll want to consider an LLC.

Ability to operate charitable programs directly

If you want to be able to create and run a charitable program that you finance yourself, it cannot be done on a tax-deductible basis out of your personal funds. This might seem strange, but there is no such thing as checkbook philanthropy when it comes to operating charitable programs yourself. Let’s say you bought an RV, stocked it with books, and began using it to run an adult literacy program. You would not be able to treat these costs as tax deductible charitable contributions. If you are planning to carry out programmatic activities, you’ll need to create a certain kind of organizational entity to do so. Private operating foundations are a common choice for this approach. In some cases, it may also be possible to do so through an LLC or a philanthropic fund. Using an LLC will confer a layer of liability protection between the donor/owner and the LLC’s activities, but as a pass-through for tax purposes, an LLC’s charitable programmatic expenses will not be deductible to its owners. Another option is to seek a fiscal sponsor arrangement with an existing public charity, such as a community foundation or well established non-profit. In this case, you will make a grant to the fiscal sponsor organization, and they administer the program under their auspices, usually charging an administrative fee for doing so. This arrangement allows you to test the waters with a new program without incurring the costs of forming an entity and seeking tax exemption.

Ability to make disbursements to fulfill personal pledges

If a significant part of what you want to accomplish involves fulfilling personal pledges you’ve already made to support one or more charitable organizations, it’s important to know that it’s not permissible to make distributions from a donor-advised fund for this purpose. Similarly, you cannot use a private foundation to fulfill a personal pledge. However, it is permissible for the foundation itself to make and fulfill a pledge.

Ability to give anonymously

There might be a variety of reasons, from privacy concerns to religious beliefs, why you’d like some of or all of your giving to remain anonymous. If anonymity is important to you, you’ll want to consider this as you set up your philanthropic structures. Some vehicles, such as donor-advised funds and LLCs, make it easy to give anonymously. Others, like private foundations, require you to list your grant recipients and grant amounts in a publicly disclosed, annual filing with the IRS.

WHERE—Where are the intended recipients of your giving based?

Domestic vs. International Grantmaking

Individuals based in the United States cannot make tax-deductible contributions from personal funds to charitable organizations based overseas. In some cases, foreign charities have US-based “Friends of” organizations which are eligible for US tax deductions. And if you operate a private foundation, you will have to undertake additional diligence requirements in order to disburse grants to non-US based organizations. Similarly, if you are vesting resources in a donor-advised fund with the intention of giving overseas, it’s important to make sure that the public charity that administers your DAF is prepared to take on these additional requirements. You may find that giving money to a philanthropic fund that specializes in international giving is an option you want to consider.

WHEN—Over what period of time do you intend to conduct your giving?

Degree of Donor Family Control Over Time

Perhaps you’re planning to give it all away in your own lifetime. Or, perhaps you intend to establish a giving program that carries on within your family over successive generations. Either way, the intended time period over which you want to disburse your resources and the degree of family control you want to maintain will have important implications for how you structure your giving. For example, the recommendation rights for a donor-advised fund can typically be passed on to one successive generation, whereas a private foundation can theoretically operate under your family’s control in perpetuity—provided your descendants can agree to get along after you’re gone!

Annual distribution requirements

This is a factor to consider if you want to have complete flexibility regarding how much you give away in any given year. For instance, private non-operating foundations are required to give away at least 5% of their net assets each year. Conversely, donor advised funds (as of this writing) have no annual distribution requirements. Some donors worry that they won’t be able to keep up with the 5% distribution requirement. This can be particularly true if they are planning to vest large amounts of additional resources into their foundation in the future. In my experience as a philanthropy advisor, grantmaking quality does not actually appear to suffer in the struggle to keep up with the 5% requirement. There are a great many amazing organizations out there that are very much in need of support, and it only takes a little bit of outreach (often to other funders) in order to find them. Furthermore, there are some provisions that allow you a grace period to comply with the 5% requirement. If this is the main reason you are hanging back from creating a private foundation, this news should come as something of a relief; you likely don’t need to worry so much about it.

Ability to change your mind and take back assets and use them for other charitable purposes

What happens if you change your mind and want to restructure your giving down the road? Will you be able to take money that you’ve already vested within one type of entity and move it to another? Some vehicles, like LLCs, are very flexible in this regard because you don’t get any charitable deduction up-front when you place resources in them. On the opposite end of the spectrum are donor-advised funds. Once you’ve claimed a charitable deduction by placing your money in a donor-advised fund, it’s no longer “your” money and you cannot get it back. In theory, you could impose certain restrictions on a gift to a donor-advised fund that would allow for you to recover funds under certain circumstances. These restrictions would be enforceable by authorities at the state level but in practice, most donor-advised funds won’t accept restricted donations. The only thing you can do with this money is make recommendations for charitable grants to the public charity to whom these resources now belong. So, if you want to retain the ability to restructure your approach to giving down the road, it’s crucial to keep this in mind.

Ability to take back assets and use them for non-charitable purposes

How sure are you that you want to give these resources away? What if you change your mind and want to use them for some other purpose, like unexpected medical expenses or some other family emergency? If you want to have the ability to redirect your resources to non-charitable purposes later on, this is a crucial consideration to build into the structure of your giving. Once you’ve taken a tax deduction for placing your resources in any kind of charitable vehicle—whether a donor-advised fund or a private foundation—you can’t take them back. The best you can do, in some cases, is move them from one charitable vehicle to another. In this case, an LLC might be your best option. It offers you the option of redirecting resources to non-charitable purposes because you are not eligible for a tax deduction until the moment that the LLC itself makes charitable contributions.

Stay tuned for part 3 of this series on structuring your giving

Stay tuned for the next post in this series which walks through the remaining three categories of functional questions in the chart: WHO, WEALTH STOCK and WHATEVER ELSE

Stay connected with news and articles

Join us to receive the latest news and updates from our team.

Don't worry, your information will not be shared, and you can unsubscribe at any time

We hate SPAM. We will never sell your information, for any reason.